It took approximately 3 days last weekend for President Trump to deviate back from his 50% EU tariff threat, and it seems it only took a phone call from Ursula von der Leyen, so we are back to square one.

More importantly, the notion of tariffs is being challenged by the US Court of International Trade as it unexpectedly blocked the bulk of Trump’s policy levies, on the grounds that he has overstepped his authority. The US administration was fast to appeal the case and tariffs were reinstated, creating even more uncertainty on the trajectory of the policy agenda. On the back of this headline, we saw a higher move in the S&P index, almost testing the 6k psychological level, but the marker was fast to fade the news. In terms of negotiations, there were news that Japan and US are working towards creating a sovereign wealth fund which will be investing in technology companies. Nothing was confirmed on an official basis and no more details were delivered. Someone would think that all this news is leaking based on a trade deal brewing soon between the two trading partners, nonetheless the clock is ticking, and we are approaching slowly towards the July 9th deadline. On another note, US Treasury Secretary Scott Bessent has pointed out that trade talks with China have stalled and may require a call between the 2 country leaders to maintain momentum.

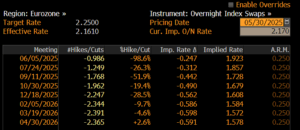

Across the pond, we had a series of CPI data which has cemented the disinflation rhetoric in Europe. Inflation in Italy and Spain eased to 1.9% in May, below the 2% ECB’s target rate. My view is that the Eurozone has a risk of under shooting it’s target of 2%, if indeed the tariff war continues or there is an escalation to it. Currently, the ECB deposit rate sits at 2.25% with 2 more cuts priced by the end of the year (see below graph)

In terms of issuance, it was a busy week with TPEIR and EUROB coming with a senior and an AT1 bond in the market. Both books were oversubscribed 8 times, which shows that there is still institutional demand for higher yielding assets. On the rates side, we saw Spain coming with a new 10yr EUR13bn issue with books closing above EUR120bn.

In equity indices, we saw a 1-2% higher move across the US and Europe with no real outperformance. Technology companies took a boost as NVIDIA results eased concerns about China with an upbeat sales forecast.

Looking ahead…

At the time of writing this newsletter, we are waiting for US Core PCE index numbers from the US. If we get an inline or below print than expectations, that could reinforce the narrative that any tariff lead inflation is transitory and we expect another leg higher in risk assets. We are entering June, bearing in mind that liquidity is going to start to diminish hence we are parking a bit more cash on carry trades and slowly taking down the beta of our portfolios, a strategy which we are following in our Athlos Balanced Strategy AMC. The year is far from over and we expect a very interesting summer given the 9th of July tariff deadline with lots of investment opportunities down the road.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.