This word has a lot of meaning and in the first 100 days of the Trump administration, it has been used by the president to describe a lot of new items in the political agenda, first and foremost, the “beautiful tariffs”. Now, there is a market argument to disagree with the adjective used around tariffs, but I guess time will show if US exceptionalism is strong enough to withstand such a volatile political agenda.

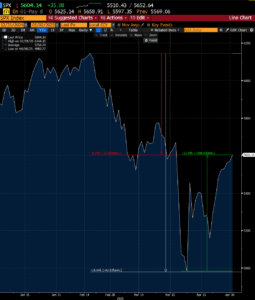

This week was a continuation of a more benign tariff narrative by the US administration, which gave another boost in the equity market. I must say that the month of April ended up higher across the board on the equity side with a 10% range across indices, something that we don’t really see very often. So, where do we stand now then? In summary, the White House has pointed out that there are multiple negotiations taking place, with India and Japan at the forefront. The market is expecting some kind of white smoke in the next 2-3 weeks which will provide guidance on what type of deals we will see forward. In the US-China front, both countries have smoothened up the rhetoric and there were multiple headlines from both sides that they will be willing to sit on the table and start the negotiation talks, given some constraints. The market’s optimism is not hard to build up and as we stand today looking at the S&P equity index we are somewhere in the middle of the range between the highs and the lows of the year (see graph below).

Furthermore, this was a week with an abundance of key data across both sides of the pond. On Wednesday, we saw US GDP Q1 numbers coming at -0.3% versus an expectation of -0.2%, alongside a higher print in Core PCE Price Index of 3.7% vs 3.1%. Stagflation fears started to mount with equity indices having a daily drawdown of up 2.5% but it was the results of Microsoft and Meta which changed the end of day rhetoric and indices ended finishing up on the day. The strength of the equity market across both sides was ratified even further with the news that US and Ukraine were about to sign a minerals deal. In Europe, we had an array of PMI and CPI data which showed better than expected results and drove European equity markets higher. As a note, DAX, the German proxy of blue-chip companies, is only trading 3.5% lower from this year’s peak and it is 14.5% higher year to date. On the results side, we saw European banks coming with a good set of numbers across the board which gave another boost on the SX7E index, up 28.5% on the year. As of now, we are all waiting for the US NFP number early afternoon with an expectation of 138k, down from 228k of last month. This will be a very important part of hard data which will show how resilient the labor market has been despite all the noise from the tariff war.

In terms of other assets, we saw EURUSD taking a breather and trading in the 1.13-1.1350 context, down from 1.1550 a week ago. Gold reversed some of the gains trading at $3257 per ounce, as a more optimistic view in the market sparked a bit of profit taking. Gold is still 24.12% higher YoY, and it has been the clear winner in terms of traditional financial assets year to date.

Looking ahead…

Next week we have the FOMC meeting on Wednesday, with the markets pricing a 6.5% probability of a rate cut. It has been obvious that there is tension between the current US administration and Fed chair, Jerome Powell. Even, the US Secretary of Treasury, Scott Bessent, an ex-hedge fund manager, mentioned in one of his interviews lately that the 2yr Treasury is pointing out to the FED Chair that he is supposed to be cutting rates. The market is split with which is the right answer here. One school of thought, is that the negative drag on growth and rise in unemployment is going to get the Fed to cut. The other is that tariffs are inflationary, hence the Fed is going to wait until further guidance. My view is that they don’t even know yet and they will wait to see consistent hard data before taking any “beautiful” decisions.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.