Tariff Truce

President Trump and President Xi agreed to extend a tariff truce, roll back export controls and reduce other trade barriers in a landmark summit. The news was celebrated by the market which traded with a strong tone across equity indices.

The US has halved fentanyl-related tariffs on Chinese goods to 10%, while China has resumed purchases of soybeans and other American agricultural products. China will also pause sweeping controls on rare-earth magnets which was a key consideration for President Trump. The agreement also includes the US extending a pause on reciprocal tariffs on China for an additional year which essentially does not solve the situation but pauses any concerns for the time being. Saying that, we have seen multiple times this year that these types of deals are quite fluid and circumstances can change at a fast and unexpected pace. The market also waited to see if President Trump will discuss any further sales of the Blackwell Nvidia chip to China but apparently this was not discussed in this meeting. As it stands now, it seems the market has accepted the period of truce with a welcoming tone, and it has now concentrated on the earnings calendar.

Speaking of earnings so far, the breath of results has been way better than expected across both sides of the pond. We are seeing US equity indices advancing on strong earnings not just from tech companies but from other industries as well, which indicate a strong fundamental prospect for next year. In Europe, banks are coming with much better-than-expected results announcing equity buy backs that will start from November onwards. All in all, we see a good set of results with constant or increasing profit margins. On the tech side, the increased expenditure in AI continues with mega scalers announcing billions of investments. So far, the market with exception of Meta Platforms is welcoming this trend as they see increased revenues from other services, especially in the Cloud software business.

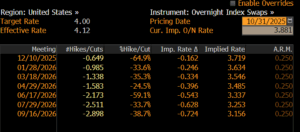

On the Federal Reserve side, the committee has lowered interest rates by 25bps as expected but Chair Powell pushed back against market expectations that a rate cut at the Fed’s next gathering in December was not a foregoing conclusion. Moreover, the Federal Reserve will stop shrinking its Treasury holdings beginning Dec 1, ending a three-year long effort, after short-term interest rates in money market remained elevated over several weeks. Markets dropped rate cut probabilities f December from 90% to 65% as shown below. The ECB kept its key interest rate unchanged, with inflation in euro area staying close to the 2% medium-term target. Currently, the markets do not expect any big deviations in policy unless data proves otherwise.

The US shutdown continues as the Congress doesn’t seem to agree on the red lines. So far, we have seen very little data away from the US CPI number that came a touch lower than expected from last week. It will be interesting to see if there is a more prolonged shutdown and how this will affect the real economy, which will be most probably shown at a later stage. More importantly, it is key in observing the trajectory of the labor market as we have seen a few companies such as Amazon announcing big cuts in workforce in the last couple of weeks.

In terms of marker performance, US equities are closing 0.5-2.5% higher with tech companies outperforming. In Europe, German stocks are under performing with DAX trading 2% lower week on week. Gold is trading around 2% lower in the week, holding its support levels of $4000 per ounce as of now. EURUSD is trading in the 1.155-1.175 context for the last month and for now it seems that this is the range it will oscillate.

Looking ahead…

On a forward basis we expect more earnings in the next couple of weeks with black out period coming to an end. What does that imply? Corporates engage into equity buybacks which will add to the positive momentum on the equity side. Furthermore, we wait to see if the US shutdown is done and dusted and what that would imply for US data, which for now seems to be a scarce resource. On a more technical note, market participants will start to consolidate positions for year end with liquidity slowly drying up and hence expecting bigger moves in pricing both ways.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.