Quarter-End Mode

It has been a while since the market had no clear direction as this week market price action felt a bit numb. We did not have any significant news from either side of the pond and published economic data reiterates what we already know.

On the tariff side, President Donald Trump plans to impose 100% tariff on branded and patented drug imports, however the market has perceived this outcome as a win for major players as most of them already have or currently building US manufacturing sites. Any locally produced products are excluded from any tariff implications. In terms of US data, GDP was revised upwards to 3.8%, estimated at 3.3% with 2Q personal consumption rising to 2.5% vs a 1.6% expectation.

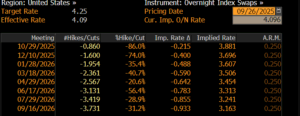

Moreover, continuing claims came lower than expected, indicating that the labor market might not be facing such a windfall. On the back of this, we have seen a reversal of US yields trading close to the 4.20% mark, around 20bps wider than the local tights. The market has dialed back some of the rates cut expectations pricing another 40bps cuts until year end, 10bps lower from last week. (see table below)

On the equity side, this week we kind of felt that we are no man’s land. End of the quarter technicals, some profit taking across the board and consolidation of positioning has caused a drop in equities as valuation worries overshadowed a good set of data which indicated that the economy is holding up well. US equities are trading 0.75-1.5% lower on the week with small capitalization companies under-performing. Similarly, in Europe we are trading 0.5% lower on average with muted flows across the board. Gold continues its positive trajectory, closing the week almost up 2%. This is another indication that the market is feeling the unease in certain factors, either through Fed independence issues or macro-political risks ahead. EURUSD has come back in the 1.165-1.175 range after the peak levels of 1.191 we saw last week during the FOMC meeting.

On other news, it seems that the US and Europe stand is consolidating with regards to the Ukraine-Russia war as there is quite a big disparity in terms of what the West wants versus what Russia is delivering. German Chancellor Merz threw his backing behind a European Union plan to leverage frozen Russian assets to provide Ukraine with an interest-free loan of nearly EUR140bn. At the same time, President Trump has publicly raised his disappointment against Putin’s stand and the lack of any positive developments.

Looking ahead…

Next week, we have another big set of data with a new quarter arising for the markets. We have PMI data from both sides of the pond which indicates the level state of the economies. More importantly, next Friday we have US Non-farm payroll with an expected value of 35k. Let me remind you that last month’s number that came much lower than expected, kickstarted a treasury rally with equities reaching new highs as the market priced in more Fed rate cuts. We continue to see upside in the market, which in our view will be more visible towards the end of October as more Q3 earnings announcements will be published.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.