If the last 2 weeks are a representation of how volatile the market will be this year, prepare yourself for a great ride. Long seems the time, when market participants were waiting for a single point of data or a speaker to point out a view, before the market moved in a disproportional way. There is a new sheriff in town though now and his political agenda dominates the news and by default the market.

The week started with a set of tariffs for Mexico, Canada (25%) and China (10%) as President Trump announced his political agenda to the market in a more aggressive way than expected. The initial reaction of the market was a weak start with EURUSD trading as low as 1.015 during early Asia hours as Canada pointed out a retaliation strategy and hitting back with a 25% levy on specific US goods. The day went by with Canada and Mexico agreeing to take tougher measures to combat migration and drug trafficking at the border, delaying the 25% tariff for a month. Risky assets bounced back with the DXY (US dollar index) weakening close to 1%. On the Asia front, China announced an investigation into Google for alleged antitrust violations and imposed new tariffs on US products. There is a tendency to believe by the market that both political parties want to negotiate a deal and avert this type of tariffs, but my gut feeling tells me that there will be a levy imposed at the end, as this is a needed new source of income which can contribute towards the US budget deficit. The worry with regards to the implementation of tariffs is quite simple to explain. Tariffs get imposed, goods become more expensive, the manufacturer passes the difference in price to the consumer hence the inflation expectations become higher. Also, as we have seen from 2018, tariffs may indeed affect negatively the growth perspective of the country and this is something that is quite important for Europe, as this is the region which still employs a budget deficit in trading terms versus the US, hence could be the next target for tariffs. In fact, President Trump has already been quite vocal that Europe’s turn is coming with some noise around the background from ECB speakers on the way they would retaliate in case those tariffs went through. Again, I don’t see how much leverage Europe has, taking into consideration the current state of growth affairs in the union.

Saying that, the start of the year was quite bullish for European stocks as the “BIG” trading strategy was the out performer. B= Bonds, I= International Stocks, G = Gold, has been the winning recipe in the last few weeks and one we have also shared across our multi-strategy portfolios and more recently the Athlos Balanced Strategy AMC.

The outperformance of European stocks year to date is something to take notice as the rhetoric of US exceptionalism has been questioned in the last week post the technology stock weakness we have recently seen. The reality is that in these markets where information and narratives change very randomly, as a portfolio manager you need to be versatile and keep liquidity in hand so you can take advantage of short-term opportunities, in other words active management hopefully provides an alpha to your strategy.

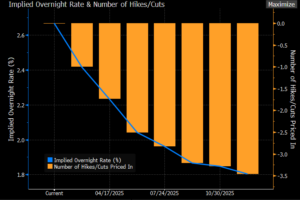

Moreover, we saw a set of PMI data coming from Europe which again pointed out the stagflationary environment that we have been in for the last few months, even though no one from the ECB council wants to admit it. European rates were the out performers this week (20bps tighter in German 10yr government bonds) with a bull 10s30s flattening on the cards and very well absorbed auctions from France and Spain. French politics seem to take a back seat for now as Prime Minister Francois Bayrou survived a no-confidence motion, ensuring the adoption of a 2025 budget after months of political turmoil. The new budget includes concessions to the socialists, with EUR52bn of savings to get a deficit of 5.4% next year and avoids shutdown. 10yr French versus German government bond spread remains above 70bps which is close to the tight of the recent range and shows some kind of relief for now in the market. More and more scrutiny is assigned towards the potential neutral rate and how ECB rate cuts should proceed given the potential implementation of US tariffs in the union. The ECB rate cut by 25bps last week came as expected and the market is currently pricing another 3.5 cuts by year end (see below table).

On the UK front, the Bank of England cut interest rates to 4.5%, a 19-month low, with 2 policymakers supporting a 50bps cut. The bank signaled a gradual approach is in play with the pound dropping and yields in UK government bonds falling as traders focused on the calls for a sharper rate reduction.

Looking ahead…

At the time of writing this note, we are waiting for the most important piece of data which arise from the US Non-Farm Payrolls (NFP) and Unemployment data. The expectation in the market is an NFP of 175k and an unemployment rate of 4.1%. There will be a lot of noise on this set of January data as a lot of seasonality factors kick in, nevertheless the market is keen to see a stable labor market combined with the disinflationary trend which was shown in the last PCE core inflation readings. For us and this is key for our investment approach, we remain tactically bullish on European rates with a blend of Global stocks and Gold. President Trump is quite vocal in terms of how he sees the world evolving in front of him. He is looking for a solution of the Ukraine-Russia war which by default will cause a fall in the price of oil. If that is the case, then the inflationary pressures from the supply side will diminish and hence US treasury yields will move tighter. Using DOGE (Department of Government Efficiency) he wants to reduce excessive government spending and by default alleviate any further expansion of budget deficits. This will allow him to cut tax rates and deregulate the banking sector. All in all, promote expansionary policies and at the same time reduce deposit rates and contract the budget deficit figures. Now, all this sounds like a great plan. Of course, if it was easy anyone could do it. There are a lot of hurdles to go through and a lot of volatility and news-flow for the market to absorb. We remain liquid with a good cash balance as the opportunity set for alpha generation is there to be exploited.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader.

This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although, Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data.