This week brought the first deal between the US and UK after a prolonged wait by the market. President Trump announced a limited trade agreement on Thursday between the two trading partners and called it as the “First of Many”.

We entered the week with a risk on tone as there was a confirmation of a meeting between the US and China political parties this coming weekend, by the Secretary of US Treasury, Scott Bessent. Global equity markets continued their move higher with an array of corporate earnings coming through across both sides of the Atlantic. One point of note here is that more than 75% of the S&P companies have announced Q1 earnings, and so far, the earnings growth stands at 12% QoQ vs an expectation of 6% QoQ. Hence, on a fundamental basis we do see issues arising from the implementation of tariffs, especially versus China, but the market’s fundamental picture, at least for now, is not as bearish as the expectations of the market.

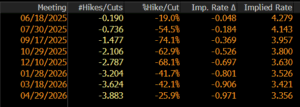

On Wednesday, we had the FOMC meeting keeping the deposit rate at 4.5% as expected. Fed Chair Jerome Powell reiterated that there is scope for more uncertainty for both inflation and employment near term trajectory. Let me remind you that the FED has a dual mandate which seeks to stabilize inflation at the 2% target level and keep unemployment levels at a low rate. He came off the Q&A meeting with a dovish stance emphasizing the strong nature of the US economy, nevertheless he pointed out that only time and data will show where the FED monetary policy path leads to. The market is currently pricing around 70bps of rate cuts by year end with a deposit rate at 3.75% (see graph below)

On Thursday, President Trump announced the first deal around tariffs versus the UK. The deal focused on reducing tariffs on cars and steel with many details to be negotiated at a later stage. The announcement gave a positive boost to the market with talks underway with Japan, India and South Korea. There was more speculation towards the end of the week, that the US administration is considering a significant tariff reduction in talks with China to ease economic pain and de-escalate tensions. According to Bloomberg, the US is aiming to reduce tariffs to 60% at first with the expectation that China will match.

On the back of the de-escalating tone, we saw EURUSD trading towards the 1.12-1.125 context after a few weeks of continued weakness. Global equities remain anchored, and we are now at “Liberation day” levels with the S&P index trading in the 5650-5700 context. European equity indices are still outperforming year to date with DAX being the outlier, up 18% on the year. We saw some profit taking in Gold, now wrapped around $3325 per ounce, up 26.67% year to date. On the rates side, European government bonds are trading 12bps off the tights with German bunds fluctuating in the 2.6-2.55% context. US 10yr Treasuries also feel quite well offered at 4.38% as the safe heaven bid has diminished for now.

Looking ahead…

Next week we have a few important data points to go through. The US CPI on Tuesday is key as the market will be looking for clues with regards to the deflationary path. Moreover, there will be headlines early next week with regards to the exploratory meeting between US and China which will define the risk tone for the week. As it stands, the market seems to be well hedged and in some respects under invested I would say, hence the pain trade for now is to see a squeeze in higher levels by equity indices. This is a view we have had for the last 2 weeks, and we see continuance in it, especially with the positive momentum currently taking place in the market.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.