Overnight, we saw Israel attacking Iran’s nuclear sites in a major escalation of tensions in the Middle East. The US administration has pointed out that this was not the ideal route as there is an upcoming meeting on Sunday between Iran and US which will focus on the former’s nuclear program and the associated sanctions relief.

Members of the IRAN parliament have pointed out that they won’t be participating in the meeting in Oman on the back of the Israeli strikes and have reiterated that the attack could not have happened without the blessing of the US administration. President Trump has mentioned multiple times that this is not his preferred route, and he wants to find a solution through discussions and not escalation. Let’s all hope this situation gets de-escalated soon as there are multiple other ways to find solutions for any issue.

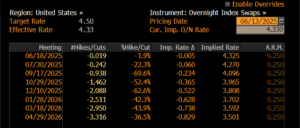

Moving on from the Middle East situation, we saw important news coming from the US administration and economy this week. First and foremost, there was an agreement between the US and Chinese authorities to establish a framework for implementing the Geneva consensus, which aims to speed up shipments of rare earth metals from China and to ease some of the US export controls. The market celebrated the outcome of the London meetings with S&P taking a leg higher, above the 6,000 level. On Wednesday, we saw US CPI readings coming lower than expected, which provided a bit more comfort in the market’s deflation perspective. Underlying US inflation rose 0.1% in May, less than what it was forecasted implying that companies are still not passing through to customers any tariff lead costs. This provided a further boost in the performance of the US 10yr treasury bond, which has traded circa 15bps tighter this week, currently at 4.35%. As we stand today, the market is pricing 2 rate cuts by year end which will take the FED deposit rate to 4%. (see below graph)

In other news, President Trump has re iterated that in the next 2 weeks, a few countries which are not currently sitting on the negotiation table will be send a letter defining the terms of their tariff deal, with an option to take it or leave it. There is more and more speculation that a deal is brewing between the US and India/Japan, nothing concrete though has been addressed. According to Commerce Secretary Howard Lutnick, the European Union is likely to be among the last deals that the US completes, as the former believes that trade negotiations could surpass the July 9 deadline. In terms of market moves, we saw a pullback in European equities, down 3-4% on the week. US equities outperforming but are still closing around 1-2% in the same timeframe. Gold continues its upward trajectory, closing the week up 3.5% at $3416 per ounce. The winner of the week though was Crude Oil, which is trading up 13.75% on the week, given the Middle

East tensions.

Looking ahead…

The Middle east escalation makes an unpredictable year even more complicated. Is this a situation of further escalation or a negotiating tactic to get Iran on the table and sign a nuclear deal? It will be very interesting to see how this rhetoric plays out during the weekend. Next week, we have the FOMC meeting with no Fed rate cut priced in. More importantly, the committee will deliver its dot plot projections with regards to forward guidance in Fed rate cuts, currently pricing 50bps. Will that change to 1 cut or remain at 2 cuts by the end of the year? Recent data supports most probably we remain at 2 cuts, but we wait to see what the Fed committee thinks of inflation pressures due to tariffs: transitionary or not?

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.