Checkmate

The winning move in a chess game always comes with one of the opponents calling a checkmate. I am not going to run ahead of myself and point out that President Trump might be soon calling “checkmate” versus his trading partners, but as of today we are in an equity market which is trading at all time highs, growth and inflation US data seems to be heading in the right trajectory and there is incoming US tariff revenue into from an effective tariff rate of around 15%.

But let’s start with the data first. We saw lower US Core CPI and PPI numbers which indicate the inflation trajectory is getting better than expected, easing a few fears of additional costs passing through to the consumer because of the new tariff regime. We also saw a massive beat in retail sales figures which indicate that the economy is running hot and the probability of a recession, as of now at least, has diminished massively. We always take these types of data with a pinch of salt as they are outdated and there is a lot of noise in terms of calculation. Nevertheless, the trend is there, and we have seen it for the first 2 quarters of the year which despite the new political regime, the US economy shows that is still quite resilient.

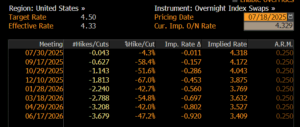

The saga with Fed Chair, Jerome Powell remains intact, with rumors that President Trump is going to fire him soon. They were of course later denied by the US administration, making the market feel a bit awkward for a short time as it seemed that this was a test to see the price action, in case this scenario was to become reality. I mean, by now most market participants are more immune to policy surprises and by default price action is much more benign. President Trump continuous the public shout out criticizing Fed Chair Jerome Powell and the need to cut rates to 1%! (we are currently at 4.5%). As of today, the market is pricing 45bps of Fed rates cuts by year end, almost in line with the Fed dot plot predictions (see below table).

Moving on, the stock market is making new record highs on both sides of the pond. There has been a heavy calendar in terms of earnings with better-than-expected results on average. US banks came in strongly with good trading P&L on FICC and Equity desks given the market volatility we saw earlier on the year. The rest of the sectors see a mixed picture as we wait for the Mag 7 to come through later in the month. US stock indices are trading 1-1.5% higher on the week outperforming their European peers. EURUSD flows seem to be a bit more balanced trading at 1.16-1.165 context, around 2% lower from the recent highs. Gold is trading 3.5% month to date with good inflows in ETFs from Asian investors. On the rates side, we have a tied trading range for now, with the German 10yr government bond anchored circa 2.7% and US 10yr Treasury circa 4.45%. The steepening trend is still there with US 10yr term premium sitting at 84bps as of today. (see below graph)

Looking ahead…

Looking forward, we wait to see more earnings coming through which will ratify the better-than-expected picture we have seen so far. On the Fed side, we have the FOMC meeting on the 30th of July which currently prices a 4.2% probability of a rate cut, despite some internal committee members advocating that it will be good to start now than later to protect the labor market. Moreover, we are getting into an illiquid period of the year as in the summer months you tend to see overshooting price action both ways.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.