“AI Jitters”

The market has been showing signs of redistribution of risk out of the technology sector into value and small cap stocks. We have also seen a redirection of risk into Europe as the fundamental lag between equity indices is obvious.

The equity price action is a clear sign that the trade rotation is taking place. S&P index is down 1% year to date along with the NASDAQ index which is trading 3% lower as well. Moreover, European equity indices are showing an outperformance of 2-5% and if we look at emerging markets that differential becomes even greater with the Japanese equity index outperforming by 15% year to date. One narrative which is picking up momentum is that AI will be disruptive in many industries such as software and for now the market is punishing any elevated valuations with a “sell first, ask questions later” mentality. If we look at how the recent earnings cycle has been, we saw healthy growth and an optimistic forward guidance. In terms of price earnings growth, the market believes that this year we will see a vertical integration of AI into different industries which will impact productivity and ultimately earnings. The positive drawback can create a lot of opportunities resulting in winners and losers, but with an overall growth in earnings alongside the S&P index.

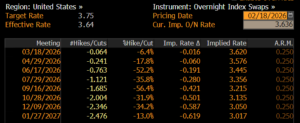

On the data side, we saw the NFP number beating estimates with an unemployment rate of 4.3%. More importantly, headline US CPI numbers came lower than expected fueling a Treasury rally of 15bps, with the 10yr bonds wrapped around 4.06%. As it stands today, the market is expecting 58bps of US rate cuts by year end (see below table).

Kevin Warsh has been appointed the new FED chair despite being regarded as one of the “hawks” in the committee. The market, for now, has not questioned the FED independence any further and at first, the appointment of Kevin Warsh has not put any further upside in risk assets. What remains to be seen is how he evolves his decision making and impact on the rest of the committee with regards to forward cuts. For now, he is keeping a neutral stand until he takes over the job at the end of May.

On the geopolitical side, we have literally forgotten about Venezuela and Greenland, and we have now concentrated on US-Iran tensions. There are talks underway regarding a nuclear deal and from what it seems there is an initial framework agreed. What remains to be seen are the final details and its implementation. On the tariff side, President Trump has started rolling back imposed levies, as the affordability perspective is becoming more important. Bear in mind, that in November we have the mid-term elections in the US as it stands today, the Democrats are way ahead in the polls. In Japan, new elections have solidified the majority in parliament of the current political party which is promising a revived fiscal policy which has helped the Japanese stock market to be one of the front leaders of performance since the beginning of the year. Furthermore, the local insurers have turned their attention towards the JGB government market as in swapped terms it makes more sense to own the local bonds rather diversifying in Treasuries or European government bonds.

In terms of price action, as we have discussed earlier, equity performance has been mixed year to date with a rotation narrative showing strong momentum for now. Credit remains strong despite tight spreads with decent demand on new issues. This is a clear indication that there is still a lot of cash parked on the side and as time goes on re investment risk grows even further. Metals, which has been an excellent diversifier for the last 2 years, continue to follow a volatile path with gold futures stabilizing close to the 5k level per ounce. EURUSD for now is trading at a tight range of 1.18-1.19 with no real catalyst in the short term but with an upward bias in the medium to long term.

Looking ahead…

There is more data in the horizon with US PCE index this week and European CPI next week. More importantly, we have NVIDIA publishing their results on the 25th of February, which is a good barometer for the technology sector and will define how the sector will be performing. On the geopolitical side, we have the Ukraine-Russia situation slowing unfolding with hopefully some green shoots in the horizon but still early to say. Nonetheless, it has been a great start of the year with a lot of volatility but with a lot of opportunities arising as there is dispersion in valuations.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.