Unleash the…Doves!

In a very predictable manner the FOMC meeting validated the dovish view the market was carrying this week and fueled even further strength in the equity market.

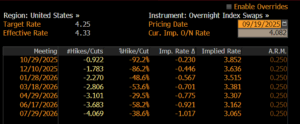

The FED committee voted for a 25bps cut in rates bringing the funds rate at 4.25% and penciled two more reductions this year. The dot plot projections were changed to 3 cuts for the year versus the June announcement of 2 cuts before. Chair Jerome Powell pointed to growing signs of weakness in the labor market to explain why officials decided it was time to cut rates. Governor Stephen Miran dissented in favor of a bigger cut (50bps) but this was largely expected by the market as he has been quite vocal about the need to move rates lower at a much faster pace. Policy makers also updated their economic projections for the years ahead seeing one quarter point cut in 2026 and one in 2027.

Despite the euphoria of the dovish FED outcome, Chair Jerome Powell pushed back against bond traders that were betting that the committee would make a series of aggressive and fast paced cuts by year end. He indicated that they are not abandoning their cautious approach due to the perceived risks of inflation. The market as of today is pricing another 57bps by year end and a full percentage point by July 2026. (see table below)

In terms of market moves, seasonality factors this year did not work out. US stocks are trading anywhere between 2.5-4.5% higher with tech companies outperforming. European stocks feel a bit more balanced in terms of flows fluctuating in the -1/+1.5% territory. The German DAX index which has a high composition in defense names has seen some profit taking given its decent run year to date, trading around -1% for the month. All in all, the rhetoric of European stocks strengthening into next year is still quite valid, as a few main street banks are updating their forecasts showing a rise of 5-10% for next year. We, at Athlos share partially that view, but we are more inclined to stay overweight US stocks as the momentum of AI and technology increase profit margins and capital expenditure in data centers will cause an out performance for next year. EURUSD is still intact in the range of 1.17/1.19 for now as some profit taking is taking place given it is a highly consensus trade. Gold has taken a breather for the time being trading at $3656 per ounce, an increase of 5.7% month to date. On the government bond side, we are trading in a very tight range across both sides of the pond. German 10yr government bonds fluctuate in the 2.65%-2.75% range and 10yr Treasuries have followed through in the 4%-4.2% context.

In Europe, we haven’t seen any change of dynamic so far as the European Commission is trying to find ways to exert more pressure on President Vladimir Putin to get him on the table which may hopefully end the Russian-Ukraine war. In the UK, data has shown that the UK government borrowing was significantly higher than the forecast in August, at GBP 18 billion. Along with a higher deficit, GBP 11.4bn higher than what the OBR forecast, the deterioration in the public finances has been driven by higher inflation pushing up spending on public services, welfare benefits and debt interest.

Looking ahead…

Next week, we continue with EU PMI data for the month of September along with US GDP figures on Thursday. Next Friday, we will get another important piece of inflation data with US Core PCE price index expected at 2.9% year to date. Let me remind you that this is the preferred set of data that is used by the FED to monitor the inflation trend. A massive deviation from this number will imply a significant market move in the rates market either way. From the companies’ fundamental perspective, we start to get Q3 earnings reports by mid-October which analysts believe will cause another strong finish to the year-end performance of the equity market.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.