The Final Countdown

We are moving closer towards the 1st of August deadline for tariff negotiations. The US administration has announced a few trade deals with Indonesia, Vietnam and Japan and they have also pointed out that there a few more in the pipeline.

The market seems to be discounting very little negative tail risk as of now, given the tariff negotiation talks. One thing is for sure, that once this is over there will be cheers and high fives across market participants, again assuming everything will end up in a market-friendly way! So far President Trump and his administration, is managing to re arrange the balance of trade across different countries facing the US market. It is obvious to us that tariffs are also a revenue generator to cover some ground towards the US budget deficit. This week President Trump announced that there is a deal signed with Japan with a 15% tariff regime and a $550bn investment commitment from Japan towards projects that the US administration will choose. The market applauded the trade deal, moving towards the recent new highs. US equities are trading 1-1.5% higher on the week outperforming its peers. Heaven assets are trading with a weaker tone, with gold unchanged on the week, at $3345 per ounce. EURUSD is fluctuating in a tied range from 1.17-1.18 with more balanced flows.

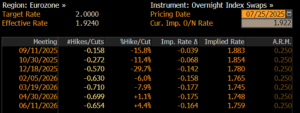

On the rates side, we had another move higher this week across both sides of the pond. The ECB meeting provided a more hawkish tone pushing European government bonds through the recent highs, with the 10yr German government bonds trading at 2.75%. Let me remind you that a week ago we were trading in the 2.58% range, and the year wide was around 2.9%. Treasuries followed through with the 10yr bond trading in the 4.42%. As it stands after the ECB meeting, the market is expecting a 30% probability of another rate cut by year end with a few main street banks calling for no more rate cuts by ECB this year. (see below graph)

In terms of earning announcements, we keep seeing better than expected results coming through. The market expectation re-earning’s growth for S&P companies sits at 5.8%, a number which can be easily beaten especially if the MAG 7 drive better than expected returns. In terms of data, we are seeing a mixed picture in Europe with regards to PMI but all in all no sign of an imminent recession. That also applies to US data, with a firm labor market and no sign of inflation moving higher, at least for now.

Looking ahead…

There has been strong momentum with regards to a EU-US trade deal with reports being issued at a 15% tariff rate. Nothing has been concluded as the market waits for a deal to be announced. Moreover, we are in the peak summer period with less issuance coming through and a few market participants taking time off. On the back of that and as usual, there is a liquidity premium attached to recent market moves which will be visible for the next 2-3 weeks. The market remains optimistic as of the trajectory of risk assets into the second half of the year, especially if the data announcements show no economic backdrop. We currently sit in the more optimistic camp of the market as for us, this is the “final countdown” before a new economic cycle starts both in Europe and the US. Have a great weekend!

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.