Big Beautiful Bill

Part 2 of the “beautiful” plan is completed as the US Congress has approved a multi-trillion dollar tax and spending bill that extends President’s Trump 2017 tax cuts, allocates resources to defense and immigration programs and reduces funding for health care and clean energy projects.

Let me remind you that part 1 of the US administration plan is Tariff implementation but before we elaborate further on this matter let’s spend a minute on the “ Big Beautiful Bill”. The bill makes significant changes to the US tax code, including extensions of individual and estate tax provisions and repealing tax credits for electric vehicles and climate projects. It is estimated to increase federal deficits by $3.4 trillion over a decade with economists warning it will add trillions of dollars to the national debt. The US administration has insisted that the bill is going to add to the growth perspective of the country which will counteract against any drag of prolonged worries on the budget deficit.

Now, moving back to the tariff saga, President Trump announced a trade deal with Vietnam. The deal includes a 20% tariff on Vietnamese exports to the US and a 40% levy on goods deemed to be transshipped through the country. In return, Vietnam has agreed to drop all levies on US imports with more details still being developed and some key aspects to be addressed. It is interesting to see if this deal will provoke any retaliatory steps from China, bearing in mind that the US has extended the truce with China and it is working to secure a deal by end of August. We are closely reaching the deadline of 9th July with a lot of unanswered questions, despite that global stocks are trading at all-time highs for this year. S&P index is trading 24% higher from the April lows with all eyes tied to the upcoming Q2 earnings. The analyst expectations lie around the 3-4% earnings growth level, again a very low barrier to beat as on average we tend to see these types of data close to the 7-8% context. In the meantime, the US administration has pointed out that they may begin sending letters to trading partners as soon as Friday, setting unilateral tariff rates, ahead of the July 9 deadline negotiations. It will be interesting to see how the market price action will evolve next week as we expect a lot of new news coming through.

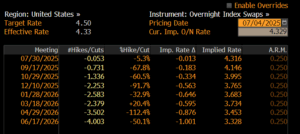

In terms of data, on Thursday, we had US non-farm payroll (NFP) numbers and US unemployment data coming through better than expected. US job growth exceeded expectations in June for a fourth straight month, and the unemployment rate fall to 4.1%. NFP increased 147,000 last month, driven by a jump in state and local government employment. Private payrolls saw a continued decline and a few street analysts pointed out that the headline NFP number is misleading as most of the labor addition was through government intakes and that on the private side the picture is much worse. Post the announcement of the numbers, the probability of a July Fed cut diminished to almost zero with still 2 cuts priced by year end, starting from September. (see below graph)

In Europe, we have had a set of PMI data which still points out to a softer picture in the economy. CPI figures also came through in line with EU expectations of 2%. In the UK, Rachel Reeves seemed to be very close to the exit door, but at a last-minute turnaround, Prime Minister Starmer gave her his vote of confidence. The UK is in a very tricky spot with stagflation fears to be quite imminent and at the same time facing a fiscal hole of 10bn+ which needs to be filled somehow, either through tax increases, lower welfare spending or increased government bond issuance. The GPB EUR pair traded as low as 1.1541 this week with UK gilts underperforming their peers.

On a weekly basis, US stocks continued their out performance closing 1.25-3% higher with small caps outperforming. European equities pointed out a bit of a softer picture trading unchanged as market participants are waiting to see further clarity with regards to trade tariffs. The EURUSD pair continues its trajectory higher, currently trading at 1.178, with a lot of analysts pointing to the 1.20 level as a good resistance point. Gold came back to its norm, adding 2% on the week and currently trading at $3342 per ounce.

Looking ahead…

We are heading to one of the most interesting weeks of the year most probably as the 9th of July tariff deadlines looms. We still don’t know how President Trump will react given there are still dozens of countries with no real trade frameworks. The market is not pricing any excess volatility at these levels as healthy inflows are taking place in both credit and equity. We are also, starting to see 2nd Quarter earnings coming through in the next couple of weeks, with the 15th of July kickstarting US bank data. It will be interesting to see which one of the two very important factors will prevail as time goes by, US earnings or tariffs. One thing is for sure, is that the market wants clarity with regards to the tariff saga as they want to become “free” from this uncertain spiral of information. And as it is 4th of July today, I want to wish everyone a “Happy Independence” day and a lovely weekend.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.