A fact which describes this year so far is that market participants don’t have the time to get bored. Away from all the tariff saga, we now face an internal argument between President Trump and Elon Musk. There was a negative market reaction with stocks erasing earlier gains on Thursday and Tesla’s stock trading 15% lower.

But let’s move on from internal affairs to market news flow and price action. The ongoing negotiations between US and China are becoming more interesting as President Trump had a call with President Xi, agreeing to further trade talks regarding tariffs and rare earth minerals. The two counterparts had a call on Thursday acknowledging that their trade relationship has derailed in a manner that is beneficial to none, stating that they are now in a better position to come up with a trade deal. The market had an initial positive reaction to the news with S&P trading at 6,000, which is a very strong psychological level. Gains were not carried out to the US session as the feud between Elon Musk and President Trump on the social platforms, caused some profit taking, especially in tech companies.

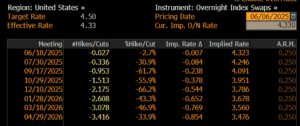

On the data side, the US Institute for Supply Management’s index of services dropped 1.7 points in May to 49.9, indicating a contraction in activity at US service providers for the first time in nearly a year. A report from ADP Research further reinforced the strain on labor, as private-sector payrolls rose just 37k last month, the least in 2 years. These are clear signs that the tariff lead initiative is causing some strain in the labor market. Let me remind you that the FED has a dual mandate, one which tackles high unemployment levels and one that maintains a 2% inflation target. The market is currently pricing 2 cuts by the end of the year, which is in line with the FED projections. (see below graph)

Across the pond, we had an array of data coming through on the CPI side. What is quite notable is that a few countries are now showcasing a CPI headline number below the 2% ECB target. On the back of this, we saw the ECB council cutting the deposit rate by another 25bps, the 8th cut in the last 18 months. We are now facing a 2% deposit rate with 1 more 25bp rate cut priced in the market by the end of the year. President Lagarde was quite vocal that the inflation fight is close to be over with the end of the cycle being imminent. I am in the camp which questions the above, as I think the risk of deflation is high and hence, I see the terminal rate lower than 1.75% by the end of the year. My assumption lies on the basic fact that I don’t see a clear-cut deal with the US and with a drag in the economy on a growth and inflation perspective due to the rolling tariffs.

In terms of market moves, we had a good week for Global stocks trading 0.75-2% higher and with US small caps outperforming. On the rates side, the US Treasury traded with a better tone, currently 10yr at 4.38% and 30yr at 4.87%. In Europe, the picture was a bit more mixed with peripheral countries trading in a more dovish manner and with the Italian – German bond spread trading at 94bps. Gold continues its upward trajectory testing $3400 per ounce this week, trading 28% higher year to date. EURUSD is fluctuating in the 1.14-1.5 context, slightly weaker from last week, a trend that doesn’t seem to be alternating in any way as the de dollarization continues.

Looking ahead…

At the time of writing this, we are expecting the US Non-Farm Payroll number (expected at 126k) which will indicate if the perceived weakness in the labor market from soft data is indeed true. Furthermore, a print of 4.2% in US unemployment is expected and anything worse than that will add to the rate cut rhetoric in a more dovish way. We think the golden case scenario here will be to have a marginally lower print in NFP with a steady 4.2% unemployment which may increase the likelihood of the FED stepping in a more meaningful way and hence increasing the market risk appetite.

Written by: Michael Konstantinou, Senior Portfolio Manager

Source: Bloomberg

The content of this Newsletter has been prepared solely for informational purposes and is not and should not be construed as a recommendation and/or advice to enter in any transactions in relation to any financial instrument or to engage in any particular trading strategy. The views and opinions expressed in this publication are solely of those of the individual author. The information contained herein is addressed to the general public and does not consider the individual circumstances, objectives or needs of any specific reader. This publication is not intended to provide tailored investment advice and should not be relied upon as such. Any person who wishes to enter into any securities transactions and/or engage in any investment activities should seek independent financial advice to assess the relevance of this information to their individual circumstances and risk tolerance. The contents of this publication are based upon or derived from information generally believed to be reliable and no representation is made as to its accuracy and completeness. Athlos Capital Investment Services Ltd accepts no liability with respect to a user’s reliability on it. Although Athlos Capital Investment Services Ltd takes reasonable measures to ensure the security of its website and newsletter content, however, it does not guarantee that the newsletter, website, or any links provided are free from viruses or other harmful digital components. Readers are encouraged to use suitable antivirus software and other cybersecurity measures to protect their devices and data. Athlos Capital Investment Services Ltd accepts no liability for any damage caused by any virus transmitted by this email. You must therefore take full responsibility for checking for viruses. Athlos Capital Investment Services Ltd reserves the right to monitor all e-mail communications.